Pricing Strategy - Perception, Value, Behavior

A Look into Pricing Strategy and Consumers

As my last three budgeting articles, a part of a series on my budgeting perspectives, have mentioned sales-volume and pricing assumptions several times, I thought it would be beneficial to work out pricing, strategy and out persistent inflation that we are all dealing with for the foreseeable future.

First, I will open up with pricing. Generally speaking, pricing is a function of marketing and a part of overall marketing strategy. The four P’s for those familiar. However, what is often overlooked, and is definitely the overarching influential factor, is the competitive economic market structure. I won’t go deeply into the theories or concepts such as economic income vs accounting income and marginal revenue vs marginal cost but understand there is much more to this topic. My paraphrasing is brief, but this brief intro will be useful for understanding pricing next time you are in your shop determining prices or out at the market wondering how a price is determined.

A quick look at 1) Economic Market Structure and 2) For P’s of Marketing Strategy:

1) Economic Market Structures

Defined by:

How many firms are competing?

How easy is it for a firm to enter into this competitive market against these firms?

Product offered and how differentiable is it to other products?

Is the product easily substituted for other products without customer loss of value?

Suggested Further Research:

Porter 5 Forces Model

Product Life Cycle

The theory is all markets will work toward equilibrium. This means if profit is to be made, firms will enter until the market share is claimed and all profit is taken by some company. Firms that can’t compete for the profit share will exit the market through bankruptcy.

Barriers might be financially based, such as an investment in equipment, resources based, such as a key mineral for production, operationally based, such as unique supply chain

Developments, or other advantages or barriers that make start-up difficult.

A) Perfect Competition

Many Competing Companies

Ease of entry into market for New Firms – Minimal barriers

Products of Minimal product differentiation

Price is necessarily competitive (low) due to the numerous options available.

-ecommerce (think of text books or eBay), farmers markets

B) Monopolistic Competition

Many Competing Companies

Ease of entry into market for New Firms – Minimal barriers

Products of Low – Medium product differentiation

Prices are competitive, but added value found in different characteristics

-most of our familiarity with markets and prices are based on -retail, restaurant, salons, clothing, grocery stores, hotels

C) Oligopoly

A Few Companies Controlling Market

Ease of entry into market for New Firms – Substantial Barriers

Products of Low - Medium product differentiation

Prices generally controlled by the firms, but influenced by market demand

-some grocery store chains (region), tires, oil, railroads, automotive

D) Monopoly

One Company Controlling Market

Ease of entry into market for New Firms – Highest level of barriers

Products of Highest Differentiation

Prices could be highest as no competitors, but this is one area often regulated

-utility companies, control market, but often government regulations

-regulations due to need (water, electricity) and price control

2) Four P’s Marketing Strategy

Product

What is begin sold? Yes, this is narrowed by industry, product-line and usage, but further by specific characteristics and perceived VALUE that a consumer believes will benefit them after purchase. The benefits could be in the promotion, ie: customer service, warranty, which is why this is a four P’s evaluation, but it is also ease of use, materials, BRAND reputation, design, desired characteristics, perhaps longevity and so on.

The primary point is the environment of competition in which the product will compete. While many products will be similar and substitutable for your particular product, are their characteristics that will separate your product from the field and are these of value that can be reflected in the price. People may pay more for an ergonometric design, or for a supplement that is proven free of heavy metals.

In economic terms most products will by within a monopolistic competition.

Position

This is ‘placing’ a product into the market amongst its direct competition. Most often, one would think of this as following the consumer perceptions of the brand that is introducing the product. Is the brand known for luxury items, high-quality industrial goods, low-cost/low-quality items and so on. This positioning of a product and its relationship to the brand is why companies often have tiers of brand names so that product lines can be introduced to the market and associated with the brand tier. Obviously, the brand can substantially influence how a product will be priced.

Cars are a perfect example. Jaguar – Ford, Lexus – Toyota … and so on. It is difficult to be a new company without a reputation and enter into a market known for a specific product or specific expectations on characteristics.

Further, this ‘placing’ also involves the distribution of the product. Do you have your own retail outlets? Do you use other retail outlets? Do you only offer products online? If you use other retail outlets, which outlets do you want to display your products? How much influence do these retail outlets hold over your product, your pricing and your promotion?

Walmart is a perfect example. Walmart holds considerable sway over products’ pricings, placement in their stores and promotions. But, if your brand is considered high-end, luxury champagne, you wouldn’t place it in Walmart.

Promotion

Marketing study and even focus groups help round out research into how the product and brand is viewed by the targeted consumer in the space of competition amongst similar products and what value can be placed on different features, relative to competitors, so that the price can be determined. But these studies also go further to determine other aspects that accompany the product that may be a contributing factor toward a purchase.

Manufacturer financing, warranties, coupons, product displays, advertising, advertising method, advertising frequency and numerous other considerations go into promotions. These offers aren’t just to entice a customer to purchase, these offers may also be with a retail chain to entice the chain to carry the product. A marketing professional would be able to add to this, but I believe the general idea is presented.

Price

Ah. Here we are. The Price. Numerous factors go into price as the aforementioned implies, but there is more to pricing. Price is both offensive and defensive. It may be used against competitors to defend market share, or it may be used to seek out new markets or increase market share. Price is as much a tool as it is used to increase operating income. Pricing is really fascinating.

While price will be influenced by the economic market structures, the product itself, and the desired positioning, we can now add a bit more detail regarding the actual customer demand that allows price to be used as a tool and how understanding customer demand is, in my opinion, the foundational block from which the rest of strategy should be built.

Understanding customer demand, requires understanding customer behavior, often defined by key socio-economic traits. Once again, since this is a social behavior that will impact usage of a limited resource (customer income), there are economic theories that help to understand how your pricing can be used to study and predict your customers’ behaviors.

You might wonder why products are often so similar and it is because there is already a known and established customer base for the product. If you know there are potential buyers, a considerable amount of risk is eliminated since you may not sell the quantity that you plan to sell, but you will probably still sell close to your planned quantity.

A brand-new product, think Apple’s Vision Pro Goggles, will require you to make educated guesses as to quantity to produce against quantity sold at a desired price and then hope that the consumer is happy with the item and not returning them for failing to meet expectations. Within the realm of technology and gaming, this strategic risk is one of the reasons pre-sales and reservations were introduced in the early 2000’s.

However, the technology industry also has a customer base that is described as the Early-Adopters. Once again, using Apple as an example, it is well known that a new product release will garner a predictable level of interest and lines of customers desiring to be the first to purchase and use the latest and greatest in technology offerings. These Early-Adopters will pay top-dollar, allowing for a quick recouping of research & development costs, just to be the first to review and gain status associated with the brand and the technology. If these Early-Adopters are satisfied, they will provide for a direct line of word-of-mouth advertising that will further drive sales. Granted, this is a combination of the cultivated branding by Apple and the behavioral traits of the technology consumers, but it does illustrate an understanding of the customer and usage of price as a tool in the real world.

So … some economic theories and representative models of customer demand and prices.

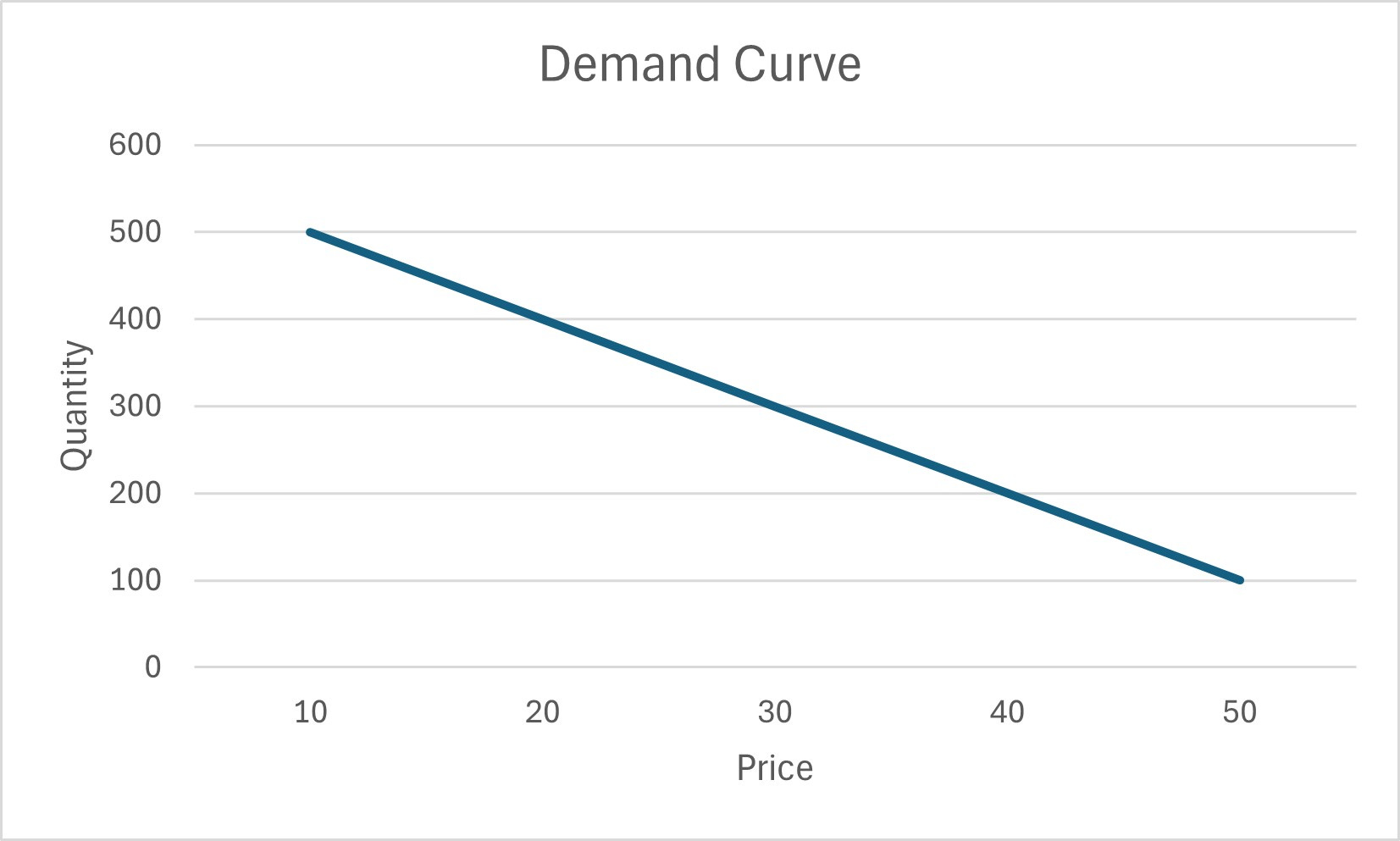

Theory of Demand

Note: there is no Theory of Supply … a Supply curve is simply used as a representation of how changes in regulatory edicts or market environment will influence a company’s willingness to produce a certain quantity of a product.

Basic Point : In a free market, over a range of possible prices for a product, as the price increases there will be a decrease in the quantity demanded.

This should be easy to understand. You would probably be willing to pay a range of prices for a certain product, but only to a certain maximum price. Anything higher than this price … nope… it isn’t worth it to YOU. This is the limit of the price paid for the value you get from the product.

This limit may be different based on YOUR INCOME and YOUR VALUE perspective of the product.

The graph of this concept

The value perspective can be defined by need, ie: water, utilities, or it might be defined by usage, ie: equipment and tools, or it might be defined by association, ie: brands and labels. If you want to look further into economic views of products and values, you can check out Luxury Goods, Normal Goods, Inferior Goods and how purchase will change based upon our next factor, Income.

Income Shift

Basic Point: Your income will dictate the quantity of a product you are willing to purchase at a given price and from which category of products (Luxury, Normal, Inferior) you will make your purchase.

It should not be a surprise that with more income you would purchase more goods that you may consider a luxury item and fewer that you would consider inferior. Think of purchasing Mac’n’Cheese vs Steak. It should also not be a surprise that you may be willing to purchase goods at a slightly higher price because you now have more income.

Price Elasticity of Demand

In order to measure the change in demand relative to a change in the price and thereby determine, using the various theories, how your customers’ view your product and even how your customers’ are doing financially in the current economic environment we can benefit by using the price elasticity of demand.

These two variables work in opposite directions for the general economic market structure. The increase in price will decrease the quantity demand. The percent change is useful because if a 1% change in price will cause a 5% decrease in the quantity demanded then you know your product is highly sensitive to price (highly elastic) and customers are not willing to pay a higher price or customers have many options for products very similar to your product. If the percent change in demand is less than the percent change in price than the product is inelastic and very well may be a necessity.

Of course, within your company someone will have to collect sales data, change prices, evaluate promotions and price specials and create an analytical environment to make use of the economic tools listed above. However, knowing at what price your customers will purchase your product, how they will react to price changes, and how they perceive the value of your product is only half the equation of pricing. We also need to understand pricing methods relative to cost of production and desired returns on investment in production. After all, your company needs to be competitive on price in order to sell your products, but if you don’t maintain a positive operating income, you won’t be solvent for very long.

Pricing Methods (in brief)

A) Cost-Plus

This method is exactly as it sounds. Determine the cost and add a margin. The cost aspect can be a littler more complex than one might assume initially. Will you use variable cost or will you use absorption cost? How will you allocate overhead? Are you using process costing or job costing, standard costing or normal costing?

When determining the margin, what will you use as the required rate of return? IRR, ROI, WACC or some flat percentage.

B) Target (Market) Pricing

This method is in-line with the positioning of the product that is mentioned in the Four P’s of Marketing Strategy. Your product is going to be placed in the competitive market and, if this market is established, you are going to have a ready list of competitors’ products and respective prices. Once known, you need to back out your margin from your respective cost to produce the product.

Since the competitive price range is established in the market, this pricing method is often used in concert with Value Engineering. That is, going through your entire value chain used in the production of the product, from design to service, and evaluating the chain for the areas that add value to the product and those areas that could be eliminated to save costs. Through this assessment of value and cost optimization, a greater margin can be worked out for the product.

Pricing is an involved activity. A good bit of analytics and a good bit of understanding of economics is useful, if not required, to create a competent and competitive pricing mechanism for a company’s products. That said, I want to add one more dynamic to this article on pricing strategy, the target customer.

Target Customer

Understanding your target customer will assist your company in planning your marketing strategy, advertising channels, product distribution channels, future product-lines and revenue forecasts. In other words, getting the most bang for your buck on all necessary cash outflows associated with selling your product and an accurate projection on future cash inflows.

It is for this reason that companies try to gather data representing their customer base. If you recall, I did hint that customer demand relative to product would reveal common socio-economic details about the general customer purchasing a product.

One of the most common errors that a company makes is believing that their product appeals to everyone. This is simply not true. If you were able to acquire socio-economic data on all of your customers, inclusive of their interests from age, income, profession, education, and home zip-code to hobbies then you would find curious commonalities for the majority of your customers.

Further, if you were able to find four or five primary characteristics then you would be able to plan out commercials, the medium to use to run commercials and perhaps even the time to run the commercials. You would discover what appeals to your customer base and be able to optimize any investments that are necessary to continue your operations. You would find benefit understanding your customers and you would find it in the data. I believe that the analytical approach to discover your target customer would be extremely useful for any company.

Companies and even customers can benefit from this data collection and analysis. Now, you do not need to invade privacy to learn about your customers and you probably already have substantial data on your customers. But if you find that you do not, ad hoc analysis can be used to draw conclusions about your customers or potential customers.

Useful Sites include (some free, some pay):

Federal Reserve Data Tracking

Bureau of Labor Statistics

Centers for Disease Control

State Employment Statistic Tracking

Real Estate Companies

Social Media Sites

University Sites

One might be surprised at the amount of data that is out there and available.

Privacy is still a primary issue when it comes to data even though we give up so much to various social media platforms. First, always respect your customers’ data. Second, that aggregate mess of data could be made useful with a few techniques such as Clustering Analysis. But that is a topic for another time..